Mobile money could add $5.3 billion to Ethiopia’s GDP

Monday 3 July, 2023

| Central Insights | Mobile for Development

Today GSMA launched its new report Mobile Money in Ethiopia: Advancing financial inclusion and driving growth. The much-anticipated liberalization of the telecoms market is presenting an opportunity to advance economic development in the country, including the financial inclusion of underserved populations via mobile money.

In this study, we look at key enablers for mobile money growth, the projected impact of mobile money services, and the use cases that present the greatest opportunities to drive adoption.

Financial Inclusion in Ethiopia

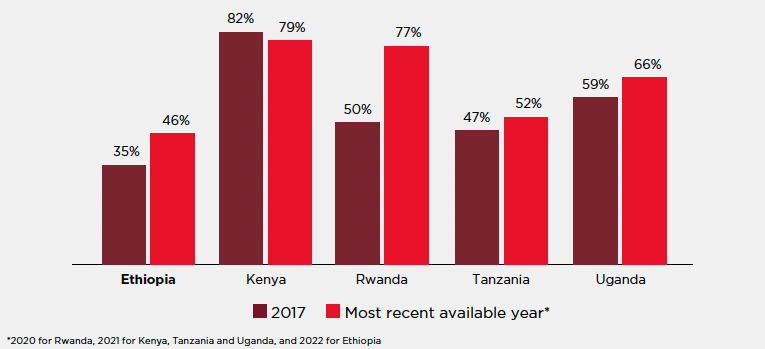

Ethiopia has notably lower financial inclusion rates than its East African neighbors. Data from Global Findex shows that less than half of Ethiopian adults had a bank or mobile money account in 2022 compared to almost 80% of adults in Kenya, 77% in Rwanda, and 66% in Uganda.

Figure 1: Formal financial inclusion in Ethiopia compared to other East African countries

Regulatory evolution and mobile money services

The financial system in Ethiopia, including digital finance, has historically been dominated by banks and micro-finance institutions. Regulatory change from 2020 has allowed non-banks to provide mobile money services. This change is part of a broader liberalization of the economy from state-led to private sector-led growth.

After liberalization, the only mobile operator in the market, state-owned Ethio Telecom launched its mobile money service telebirr in May 2021, rapidly scaling up subscriptions. Safaricom has also entered the market, and, in May 2023, obtained a mobile money license. In addition, the government of Ethiopia plans to privatize 45% of Ethio Telecom as well as admit another mobile operator into the market. If all goes to plan, by 2025 Ethiopia should have three mobile operators offering mobile money services.

A competitive market could be a game-changer for financial inclusion. In Kenya, Ghana, and Uganda, mobile operators have been able to leverage wide subscriber bases, large distribution networks, and trust in their brands to reach a significant proportion of financially underserved populations via mobile money.

Projected impact of mobile money services

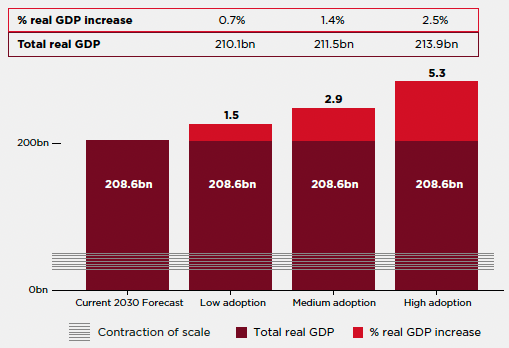

As part of our research on how to scale mobile money in Ethiopia and the socio-economic benefits this can bring, GSMA Intelligence forecast the positive impacts of mobile money adoption on poverty reduction, GDP growth, tax collection, and resilience to economic shocks in the country.

GSMA Intelligence estimates that should Ethiopia see high adoption of mobile money, i.e., approximately 60% of Ethiopian adults are mobile money users by 2030, mobile money could:

- Lift 700,000 people out of extreme poverty.

- Add $5.3 billion to Ethiopia’s GDP.

- Increase tax revenue by $300 million.

- Provide a cushion for the economic shocks experienced by almost 40% of Ethiopian households.

Figure 2: Modelled GDP impact of mobile money growth by 2030

Whether Ethiopia will see high adoption of mobile money, however, depends on a number of enabling factors, listed below:

- Connectivity

- Affordability

- Policy/regulations

- Literacy and digital skills

- Payments interoperability

- Awareness, trust, safety, and security

- Access points and agent networks

- Product relevance

- Use cases

Our report discusses these factors in detail. In this blog, we highlight three: access points and agent networks; affordability of handsets and mobile services; and relevant use cases.

Access points and agent networks

Ethiopia’s regulations are becoming increasingly enabling, and payment interoperability is steadily advancing, which will provide impetus to scaling mobile money services.

Ethiopia also benefits from relatively good network coverage, with 99% of the population covered by a mobile network, according to the latest information by Ethio Telecom. However, network quality is unreliable and transactions are frequently disrupted, acting as a deterrent to mobile money adoption and use. Electricity is also a significant challenge with only 51% of Ethiopians having electricity in 2021.

Low access to banking points continues to be one of the biggest challenges to financial inclusion. According to data from Global Findex (2022), almost 20% of adults do not have a bank or mobile money account because financial institutions are too far away. A core focus of mobile operators entering the market will be to build out a trained and incentivized agent network to ensure onboarding and training of customers.

Investing in managing and training agents, offering mutually beneficial commission structures and faster vetting to register agents will be an expensive proposition requiring the deployment of patient capital. However, this will be for a crucial step for driving mobile money adoption, especially in rural areas where 79% of the population live.

Affordability of handsets and mobile services

Despite mobile money services having been offered in Ethiopia since 2015 by banks and micro-finance institutions, and in the last two years by Ethio Telecom, Findex data (2022) indicates that only 5% of men and 4% of women have a mobile money account.

One factor that accounts for low uptake is the affordability of mobile phones and services. According to the Alliance for Affordable Internet (A4AI), the cost of a smartphone is particularly significant and represents almost 97% of average monthly income in Ethiopia. Strategies to make mobile phones more affordable, such as easy availability of low-cost smart feature phones and device financing may improve handset affordability.

As an additional barrier, while mobile services in Ethiopia are offered at competitive rates compared to other regional markets, they are still expensive relative to income compared to services in the Asia Pacific and Europe, putting a strain on low-income populations.

Relevant use cases

Prioritizing use cases that will scale in the short run will likely provide commercial sustainability in the immediate term, while mobile money providers build their readiness to expand the value proposition of mobile money in the longer term. Our research shows that besides the “usual” entry points to mobile money such as cash in-cash out, and person-to-person transfers, the digitalization of government-to-person (G2P) and person-to-government (P2G) payments is a key opportunity to drive the adoption and usage in the short run.

The government recognizes the role that G2P/P2G use cases can play in financial inclusion and has been digitalizing P2G payments such as for traffic violations, and has also mandated digital-only payments for fuel purchases. In addition, mobile banking service CBE Birr and Telebirr are facilitating bill payments for government-managed utility services, such as water and electricity.

As the ecosystem matures, mobile money will also become a viable option for international remittances, merchant, agricultural and humanitarian payments. With most Ethiopians saving at informal institutions, low accessibility and uptake of credit, and almost no instances of insurance products for agricultural communities or microentrepreneurs, tailored micro-credit, micro insurance, and micro-savings products are another prominent opportunity. Microfinance products however require greater ecosystem maturity, especially when it comes to partnerships with financial service providers.

The importance of consumer confidence, trust, and security

In focus group discussions we conducted with mobile money users in Ethiopia, trust, safety, and security were indicated as notable barriers to regular use of services, linked to low financial and digital literacy, poor network quality, and concern over the smooth functioning of technology.

A notable number of focus group participants said they avoided using mobile money agents due to low trust in the system’s agents used to carry out transactions. While digital and financial literacy will help build trust, robust cyber-security and clear and efficient redress mechanisms for fraudulent or erroneous transactions, where the liability rests with the provider, would all be crucial elements for the adoption of mobile money by building confidence in the service.

To understand the current landscape and opportunity for mobile money in Ethiopia, read our new report.

About Addis Insight

Addis Insight is Ethiopia’s fastest growing digital news platform, providing consumers with the latest news from Ethiopia and its diaspora. We provide marketers with innovative opportunities to leverage our stories and overall brand with a fiercely curious and highly engaged audience.